Emergency Fund Calculator: How Much Should You Save in 2026?

Calculate your 2026 emergency fund target using updated guidelines. Learn why 6-12 months of expenses is now recommended and get step-by-step savings strategies.

Most financial experts recommend saving 3-6 months of essential expenses in your emergency fund, but in 2026's economic climate, 6-12 months is often more appropriate. Calculate your target by multiplying your monthly essential expenses by your risk factor (3-12 months based on job stability, dependents, and income variability). Think of your emergency fund as your financial airbag — you hope you never need it, but when life hits you unexpectedly, you'll be grateful it's there.

Remember when someone first explained how a savings account works? Understanding how much you need in your emergency fund is just as straightforward once you see the formula. The tricky part isn't the math (honestly, it's pretty simple) — it's figuring out your personal situation and what 2026's economy means for your safety net.

- 2026 emergency funds should cover 6-12 months of expenses (up from the old 3-6 month rule)

- Calculate by multiplying monthly essential expenses by your personal risk multiplier

- High-yield savings accounts earning 4-5% are ideal for emergency fund storage in 2026

- Build your fund gradually — even $500 is better than nothing to start

How Much Should You Save in Your Emergency Fund in 2026?

Let me connect this to something you already know: You wouldn't drive without insurance, right? Your emergency fund is financial insurance. But unlike car insurance with fixed premiums, your emergency fund size depends on your unique situation.

The 3-6 Month Rule Updated for 2026

That old "3-6 months" rule? It's gotten a serious upgrade. Here's the thing — 2026 isn't your grandmother's economy. With inflation still affecting everything from groceries to gas, and job markets more unpredictable than ever, financial advisors are now recommending 6-12 months of expenses.

Why the change? Simple.

Job searches take longer now. The average job search in 2026 takes 4-6 months compared to 2-3 months pre-pandemic. Plus, if you get laid off, good luck finding something at the exact same salary immediately. Most people take a temporary pay cut when switching jobs unexpectedly.

In 2026, 67% of Americans who experienced job loss took more than 5 months to find comparable employment, according to Bureau of Labor Statistics data.

Factors That Determine Your Emergency Fund Size

Think of it like this: your emergency fund isn't one-size-fits-all, just like your shoe size isn't universal. Here are the main factors that determine your number:

Income Stability — If you're a government employee with tenure, 6 months might work. Freelance graphic designer? You're looking at 12 months, minimum.

Dependents — Single with no kids? More flexibility. Supporting a family of four? You need that bigger cushion (trust me on this one).

Health Considerations — Chronic conditions or expensive medications bump up your needs significantly.

Industry Volatility — Tech workers learned this lesson hard in 2022-2023. Some industries are just more prone to layoffs.

Emergency Fund Calculator Formula

Okay, so here's the actual math (don't worry, it's easier than calculating a tip):

Emergency Fund Target = Monthly Essential Expenses × Risk Multiplier

That's it. Really.

Quick Summary: Emergency Fund Essentials for 2026

Key Takeaways at a Glance

Let's make this super practical: If you take nothing else from this article, remember these three things:

First, aim higher than you think. The old rules don't apply anymore. Second, start somewhere — even $25 a week adds up faster than you'd expect. Third, keep it accessible but not too accessible (more on that later).

Emergency Fund Benchmarks by Income Level

Here's a real-world analogy that makes this click: your emergency fund should grow with your lifestyle, just like your wardrobe probably got more expensive as your salary increased.

If you make $50,000 annually, your essential monthly expenses might be around $3,000. That means your target emergency fund sits between $18,000-$36,000 depending on your risk factors.

Making $100,000? Your expenses probably run closer to $5,500 monthly, putting your target at $33,000-$66,000.

I know those numbers look scary. But remember — you're not building this overnight.

Action Steps to Get Started

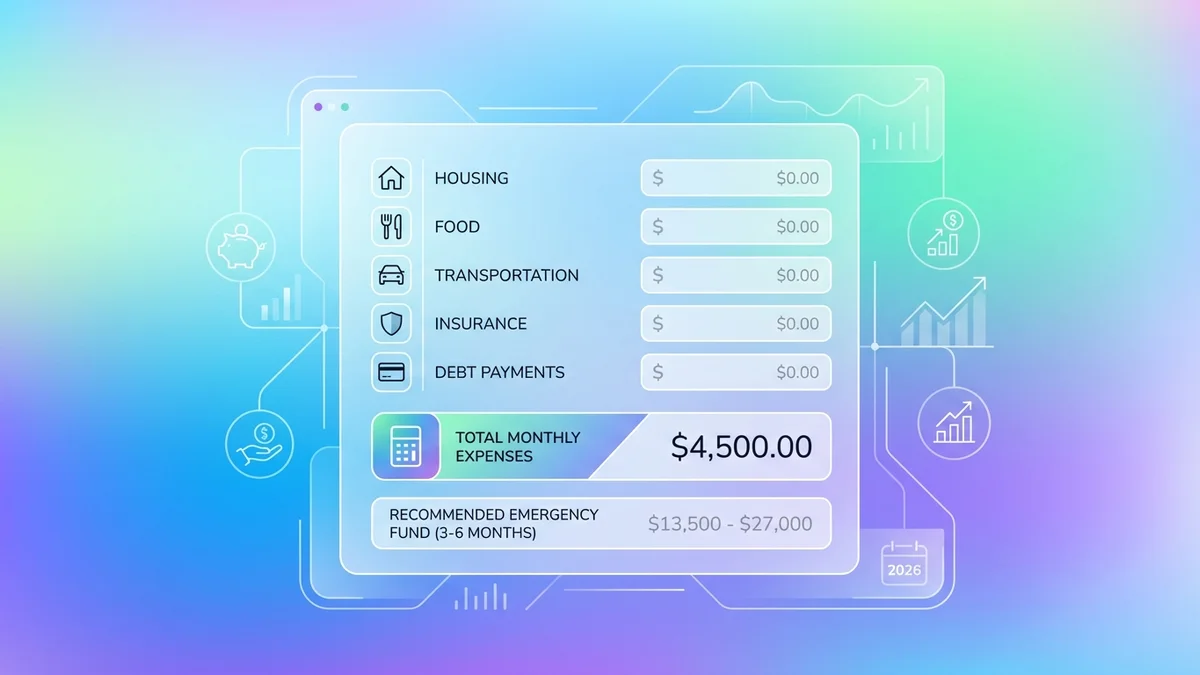

Track your spending for one month, then separate needs from wants. Include rent, utilities, groceries, minimum debt payments, insurance, and transportation. Skip the Netflix subscription and daily Starbucks runs for now.

Honestly assess your job security, health situation, and family responsibilities. When in doubt, err on the side of caution — it's better to over-save than under-save for emergencies.

Start with whatever amount doesn't hurt. Even $50 per paycheck builds momentum. You can always increase it later as your income grows or expenses decrease.

Why Emergency Fund Requirements Changed in 2026

Post-Pandemic Economic Landscape

Look, nobody saw 2020 coming. But smart people learned from it.

The post-pandemic world taught us that "stable" jobs aren't always stable, supply chains break down (remember the toilet paper shortage?), and emergencies often come in waves, not isolated incidents.

In 2026, we're still dealing with the aftermath. Remote work changed everything — sometimes in good ways, sometimes not. Companies got comfortable with layoffs. The gig economy exploded. Traditional career paths... well, they're not so traditional anymore.

Many financial advisors still quote pre-2020 emergency fund recommendations. Make sure you're getting updated advice that reflects current economic realities.

Rising Cost of Living Impact

Here's the thing about inflation — it's sneaky. You don't notice it day-to-day, but over months and years, it adds up significantly.

Your $3,000 monthly expenses in 2022? They're probably closer to $3,600 now. That 20% increase means your emergency fund needs to grow proportionally, or you're actually less prepared than before.

Housing costs hit particularly hard. Rent increases, property tax hikes, homeowners insurance spikes — your biggest expense category probably got bigger, whether you upgraded your lifestyle or not.

New Employment Market Realities

The job market in 2026 is weird (and I mean that in the most technical sense possible).

On one hand, unemployment is relatively low. On the other hand, mass layoffs happen regularly, especially in tech. Companies hire fast and fire faster. Job hopping became normal, but so did sudden "restructuring."

Plus, the skills required for jobs change rapidly now. You might need time between jobs not just to find something, but to learn new skills or get additional certifications.

Your emergency fund isn't just unemployment insurance — it's career transition insurance.

Emergency Fund Calculator: Step-by-Step Guide

Calculate Your Monthly Essential Expenses

Now, don't let this term scare you — "essential expenses" just means the stuff you absolutely cannot skip if you lost your income tomorrow.

Think of it like this: if you were suddenly broke, what bills would you still need to pay to keep a roof over your head and food on the table?

Housing: Rent or mortgage, property taxes, basic utilities (electricity, water, heat). Skip the premium cable package.

Food: Groceries for basic meals. Not restaurant dining, not organic everything, not the fancy coffee beans.

Transportation: Car payment, insurance, gas, or public transit costs to get to job interviews.

Insurance: Health insurance premiums you'd pay out-of-pocket, basic life insurance.

Minimum Debt Payments: Credit cards, student loans, personal loans — the absolute minimum to avoid default.

Essential Services: Basic phone service, minimal internet (you need this for job searching).

Determine Your Risk Multiplier

This is where it gets personal. Your risk multiplier determines whether you multiply those monthly expenses by 6, 8, 10, or 12.

- Stable government or healthcare job

- High-demand skills in growing industry

- Dual-income household

- No dependents or health issues

- Strong professional network

- Freelance or contract work

- Volatile industry (tech, media, retail)

- Single income supporting family

- Chronic health conditions

- Specialized skills with few job options

Apply the 2026 Emergency Fund Formula

Let's walk through some real examples, because math is always easier with actual numbers:

Example 1: Sarah, Marketing Manager

Monthly essentials: $4,200

Risk factors: Stable corporate job, married (dual income), no kids

Multiplier: 6 months

Emergency fund target: $25,200

Example 2: Mike, Freelance Developer

Monthly essentials: $3,800

Risk factors: Irregular income, single, supports elderly parent

Multiplier: 12 months

Emergency fund target: $45,600

Example 3: Jennifer, Recent Graduate

Monthly essentials: $2,100

Risk factors: Entry-level job, student loans, living with roommates

Multiplier: 8 months

Emergency fund target: $16,800

Start with a smaller goal first. If your target is $30,000, aim for $5,000 initially. Reaching mini-milestones keeps you motivated and builds the saving habit.

Emergency Fund Size by Life Situation

Single vs. Dual Income Households

Here's a real-world analogy that makes this click: single-income households are like driving without a spare tire. When something goes wrong, you're stuck.

If you're single or the sole breadwinner, losing your job means 100% income loss. Dual-income families have built-in backup — if one person loses their job, the other's income continues (assuming they don't work for the same company or industry).

Single-income recommendations: 10-12 months minimum. You're carrying all the financial risk, so you need a bigger cushion.

Dual-income recommendations: 6-8 months often works, but consider what happens if you both lose jobs simultaneously (it happened a lot during 2020).

Self-Employed and Freelancers

Okay, so freelancers and self-employed folks — you need the biggest emergency funds, hands down. Your income is unpredictable on a good day.

Think about it: when you're employed, getting fired is a specific event. When you're freelance, "emergency" might mean your biggest client doesn't renew, or economic conditions make everyone tighten budgets, or your industry hits a slow season.

For self-employed individuals, I recommend 12-18 months of expenses. Yes, eighteen months. I know that sounds like a lot, but irregular income requires irregular preparation.

Plus, you don't qualify for unemployment benefits in most states. Your emergency fund IS your unemployment insurance.

Parents and Family Considerations

Kids change everything financially (shocking revelation, right?).

Not only do children increase your monthly expenses, but they also increase your emergency expense potential. Kids get sick more often. They need things at inconvenient times. School situations change. Childcare costs are astronomical and often non-negotiable.

Parents should add 2-4 months to their base emergency fund calculation. So if your risk factors suggested 8 months, bump it to 10-12 months with kids.

Also, consider this — if you lose your job, you might save on childcare costs temporarily, but you'll need extra funds for health insurance premiums if you lose employer coverage.

Real-World Emergency Fund Examples and Case Studies

Case Study: Tech Professional Emergency Fund

Meet Alex, a software engineer in Austin making $95,000 annually. In early 2023, Alex thought a 3-month emergency fund was plenty. Then the tech layoffs hit.

Alex's original plan:

Monthly expenses: $4,500

Emergency fund: $13,500 (3 months)

Seemed reasonable for a "stable" tech job

Reality check: Alex got laid off in March 2023. The job search took 8 months due to market oversaturation. Unemployment benefits covered roughly 40% of previous income. The emergency fund lasted about 6 weeks.

Alex's new plan for 2026:

Monthly expenses: $4,800 (adjusted for inflation)

Emergency fund target: $57,600 (12 months)

Current progress: $31,000 saved

Alex learned that even "stable" industries aren't immune to mass layoffs, and job searches in competitive fields take longer.

Case Study: Small Business Owner Savings Strategy

Maria runs a small marketing consultancy. Her income varies wildly — some months she makes $8,000, others just $2,000.

Maria's challenge: How do you calculate emergency fund needs when your income isn't steady?

Maria's solution:

She calculated based on her minimum required personal draw: $3,500/month

Business emergency fund: 6 months of business operating expenses ($18,000)

Personal emergency fund: 18 months of personal expenses ($63,000)

Total emergency savings: $81,000

Sounds like overkill? Maria's business survived the 2024 recession when many competitors folded. During slow periods, she focused on business development instead of panicking about money.

Small business owners need both business and personal emergency funds. Business emergencies (equipment failure, major client loss) are separate from personal emergencies.

Case Study: Recent Graduate Starting Out

Jake graduated college in May 2025 with $32,000 in student loans and a $45,000 starting salary. Building an emergency fund seemed impossible with loan payments and basic living expenses.

Jake's strategy:

Started with a micro-emergency fund: $1,000

Built it gradually: $100/month automatic transfer

Used tax refund and birthday money for boosts

Reached $5,000 by March 2026

Jake's wake-up call: Car transmission failure in January 2026 cost $2,800. Without the emergency fund, Jake would've needed credit cards or payday loans.

Current status: Jake's rebuilding the fund and aiming for $15,000 (8 months of bare-bones expenses) by end of 2026.

The lesson? Start small, but start immediately. Even $1,000 handles most minor emergencies.

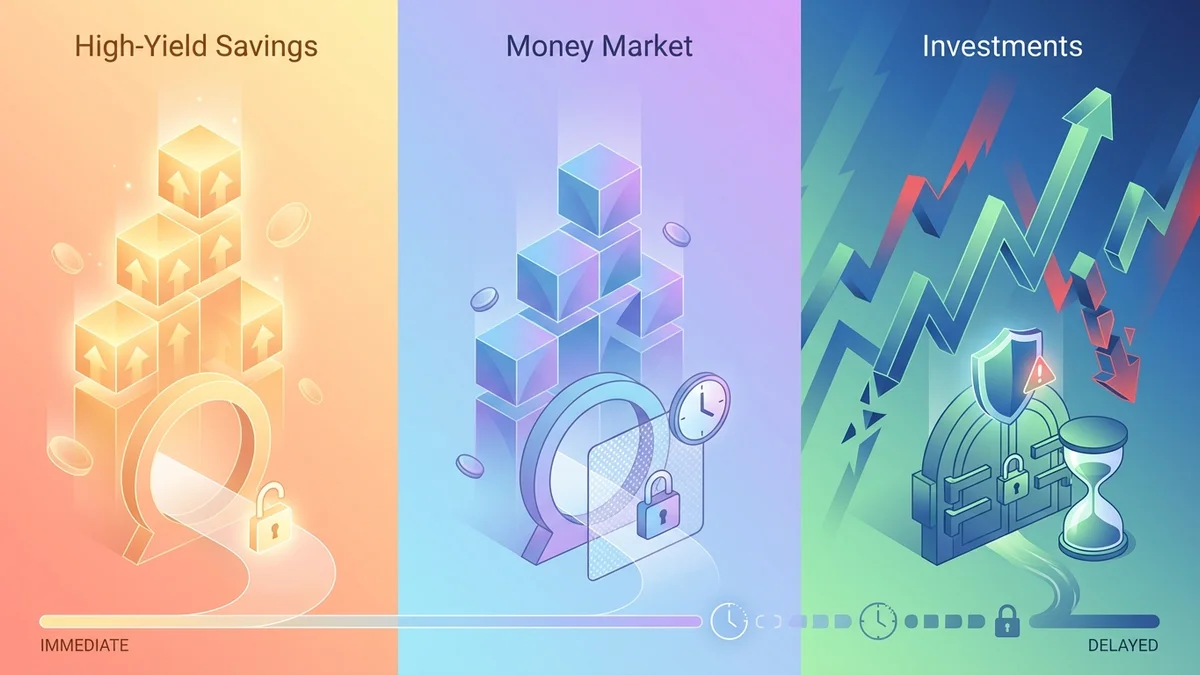

Best Places to Keep Your Emergency Fund in 2026

High-Yield Savings Accounts Comparison

Let's make this super practical: your emergency fund needs to be boring. This isn't investment money — it's insurance money.

In 2026, high-yield savings accounts are paying 4-5% annually, which actually keeps pace with inflation (finally!). The key features you want:

FDIC Insurance: Non-negotiable. Your emergency fund must be guaranteed safe.

Easy Access: You should be able to transfer money to checking within 24 hours, max.

No Minimum Balance Penalties: Emergency funds fluctuate as you use and rebuild them.

Competitive Rate: Aim for accounts paying at least 4% in 2026's interest rate environment.

| Bank Type | Average Rate | Pros | Cons |

|---|---|---|---|

| Online Banks | 4.5-5.2% | Highest rates, low fees | No physical branches |

| Credit Unions | 3.8-4.5% | Member benefits, good service | Limited ATM networks |

| Big Banks | 0.5-1.5% | Convenient locations | Terrible interest rates |

Money Market vs. CDs for Emergency Funds

Here's the thing about Certificates of Deposit (CDs) — they pay slightly higher interest but lock up your money. That defeats the whole purpose of emergency fund accessibility.

Money market accounts split the difference. They typically pay rates between regular savings and CDs, while maintaining reasonable access through debit cards or checks.

- Higher interest than regular savings

- Debit card and check access

- FDIC insured

- Rate flexibility with market changes

- Higher minimum balances

- Limited monthly transactions

- Rates can decrease

- More complex fee structures

My recommendation? Stick with high-yield savings for simplicity. The rate difference isn't worth the complications for emergency funds.

Accessibility vs. Growth Balance

Think of it like this: your emergency fund is like keeping a fire extinguisher in your kitchen. You want it to work perfectly when needed, even if it just sits there most of the time.

Some people get tempted to invest emergency funds in stocks or crypto for higher returns. Don't do this. When emergencies hit, markets are often down too (2020 and 2022 proved this dramatically).

The "growth" in your emergency fund comes from interest and from avoiding debt during emergencies. If your $20,000 emergency fund saves you from $20,000 in credit card debt at 24% interest, you just "earned" $4,800 annually in avoided interest.

Your emergency fund's job isn't to make you rich — it's to keep you from going broke.

Building Your Emergency Fund: Practical Strategies

Automated Savings Plans

Honestly, if you're trying to build an emergency fund through willpower alone, you're probably going to fail. Not because you lack discipline, but because life gets busy and manual savings get forgotten.

Automation is your friend. Set up automatic transfers from checking to your emergency fund savings account. Treat it like a bill that has to be paid.

The "Pay Yourself First" Strategy:

Transfer money to emergency fund immediately after payday, before you pay other bills or spend on discretionary items. Even $50 per paycheck adds up to $1,300 annually.

The "Round-Up" Strategy:

Many banks now offer programs that round up purchases to the nearest dollar and save the difference. Buy coffee for $4.65? They'll charge $5.00 and save the $0.35. It's painless and automatic.

The "Percentage" Strategy:

Save a fixed percentage of every paycheck. Start with 5% if money's tight, increase to 10-15% as you get comfortable.

Side Hustle Income for Emergency Funds

Here's a strategy that works surprisingly well: dedicate side hustle income entirely to emergency fund building.

Your main job covers living expenses. Side income builds financial security. This mental separation makes it easier to save because you're not "taking" money from your lifestyle.

Popular 2026 side hustles for emergency fund building:

- Food delivery (flexible hours, immediate income)

- Online tutoring or consulting (leverage existing skills)

- Selling items you no longer need

- Freelance writing or design projects

- Part-time retail during busy seasons

Even an extra $200 monthly from side work builds $2,400 annually toward your emergency fund.

Open a separate savings account specifically for emergency funds. Mixing emergency money with regular savings makes it too easy to justify spending it on non-emergencies.

Tax Refund and Windfall Allocation

Tax refunds, work bonuses, gifts, insurance settlements — windfalls are emergency fund goldmines if you handle them right.

The temptation is always to spend windfalls on fun stuff. That's human nature. But here's a compromise that works: split windfalls 70/30 between emergency fund and discretionary spending.

Got a $2,000 tax refund? Put $1,400 toward emergency fund, spend $600 on something you enjoy. You're building security while still treating yourself.

For smaller windfalls (under $500), consider going 100% to emergency fund until you reach your target. For larger ones (over $5,000), maybe do 80/20 to make the savings feel less painful.

Frequently Asked Questions About Emergency Funds

Common Misconceptions Debunked

"Credit cards can serve as my emergency fund" — This is dangerous thinking. Credit cards mean you're borrowing money at high interest rates during your most financially vulnerable time. Plus, credit limits often get reduced when you need them most.

"I'll just borrow from my 401(k)" — 401(k) loans seem convenient but come with risks. If you lose your job, the loan typically becomes due immediately. You're also missing out on investment growth during repayment.

"Three months is plenty in 2026" — This outdated advice doesn't reflect current economic realities. Job searches take longer, costs are higher, and economic volatility is greater than pre-2020.

Emergency Fund vs. Other Financial Goals

This is where prioritization gets tricky. You've got student loans, you want to invest, maybe you're saving for a house. Where does emergency fund rank?

Generally, financial advisors recommend this priority order:

1. Build mini-emergency fund ($1,000-$2,500)

2. Pay off high-interest debt (credit cards over 15% interest)

3. Build full emergency fund

4. Invest for retirement and other goals

The logic: without an emergency fund, any financial setback forces you back into debt, undoing progress on other goals.

When and How to Use Your Emergency Fund

Real emergencies are typically unexpected, necessary, and urgent. Here's the test: Is this expense all three?

True emergencies: Job loss, major medical bills, essential home repairs (heating system failure), car repairs needed for work transportation.

Not emergencies: Christmas gifts, vacations, wedding expenses, "great deals" on non-essential items, predictable expenses like annual insurance premiums.

When you do use emergency funds, prioritize rebuilding them immediately. Cut discretionary spending temporarily and direct that money back to the emergency fund.

Emergency fund "creep" is real — once you have money sitting there, it's tempting to justify using it for non-emergencies. Stay disciplined about what qualifies as a true emergency.

Building an emergency fund in 2026 isn't just smart — it's essential for financial survival. Start with whatever amount doesn't stress your monthly budget, even if it's just $25. The habits matter more than the initial amount.

Your future self will thank you when life throws those inevitable curveballs. And trust me, they're coming — they always are.

Ready to start building your emergency fund? Calculate your target amount using the formula we covered, then set up that automatic transfer today. Even small steps forward beat standing still, and every financial expert started exactly where you are now — at the beginning.

Frequently Asked Questions

1How much should I have in my emergency fund in 2026?

2What counts as an essential expense for emergency fund calculations?

3Should I pay off debt or build my emergency fund first?

4Where should I keep my emergency fund in 2026?

5How long does it take to build a full emergency fund?

6Can I use my 401(k) as an emergency fund?

Enjoyed this article?

Share it with your network

Related Articles

Debt Snowball vs Debt Avalanche: Best Strategy for 2026

Discover which debt payoff method saves more money and which one you'll actually complete. Compare snowball vs avalanche strategies with real 2026 case studies.

What is Dollar-Cost Averaging? Best Strategy for 2026

Learn how dollar-cost averaging removes market timing stress and builds wealth automatically. Simple strategy, powerful results for 2026 investors.